About us

About us Who We are

Who We are Our Products

Our Products E-books

E-books Contact us

Contact us Skilled Tasker

Skilled Tasker Speedo Delivery

Speedo Delivery Best Match

Best Match Locate Bee

Locate Bee Hire Flutter Developer

Hire Flutter Developer

Hire Hybrid Developer

Hire Hybrid Developer

Hire Android Developer

Hire Android Developer

Hire Frontend Developer

Hire Frontend Developer

Hire ReactJS Developer

Hire ReactJS Developer

Hire NodeJS Developer

Hire NodeJS Developer

Hire Xamarin Developer

Hire Xamarin Developer

Hire iOS Developer

Hire iOS Developer

Hire WordPress Developer

Hire WordPress Developer

Power BI

Power BI

Power Pages

Power Pages

Copilot Studio

Copilot Studio

Power Automation

Power Automation

Power Apps

Power Apps

Power Virtual Agents

Power Virtual Agents

Developer Tools

Developer Tools

Databases

Databases

DevOps

DevOps

Identity

Identity

Integration

Integration

Management and Governance

Management and Governance

Internet of Things

Internet of Things

Migration

Migration

Mobile

Mobile

Security

Security

Web

Web

Analytics

Analytics

Sales

Sales

Marketing

Marketing

HR

HR

Supply Chain Management

Supply Chain Management

Intelligent Order Management

Intelligent Order Management

Flutter Development

Flutter Development

Ionic Development

Ionic Development

Angular JS

Angular JS

JavaScript

JavaScript

Wearable

Wearable

AR VR

AR VR

MongoDB

MongoDB

Amazon Web Services

Amazon Web Services

MySQL

MySQL

User Experience

User Experience

User Interface and Evaluation

User Interface and Evaluation

User Experience Review

User Experience Review

Digital Marketing

Digital Marketing

Social Media Marketing

Social Media Marketing

PPC

PPC

SEO

SEO

IT consultation services

IT consultation services

Dev Ops

Dev Ops

Launching and Growth Hacking

Launching and Growth Hacking

Scope of Work

Scope of Work

Product Discovery Workshop

Product Discovery Workshop

Strategic Business Analysis

Strategic Business Analysis

Food And Beverage

Food And Beverage

Banking and Financial

Banking and Financial

Travel and Tourism

Travel and Tourism

Oil and Gas

Oil and Gas

Energy and Utility

Energy and Utility

E-commerce

E-commerce

Media and Social

Media and Social

Healthcare

Healthcare

Hospitality

Hospitality

Education

Education

Real Estate

Real Estate

Customer Support

Customer Support

Lead Generation

Lead Generation

Appointment Setter

Appointment Setter

E-Commerce

E-Commerce

Traditional risk assessment and claims management methods face several significant challenges that highlight the need for modern solutions:

Many problems are only identified after extensive damage has already occurred. For example, a burst pipe in a home might go unnoticed until considerable water damage has happened, leading to higher repair costs and a more complex claims process.

Filing and managing claims can be slow and cumbersome. Customers often experience long wait times and complicated procedures, which can lead to frustration and diminished trust in their insurer.

Conventional systems frequently lack real-time monitoring and data collection capabilities. This results in insurers working with outdated or incomplete information, impacting the accuracy of risk assessments and claims decisions.

The Internet of Things (IoT) provides practical solutions to these issues by integrating modern technology that enhances risk assessment and streamlines claims processing. IoT devices enable real-time data collection, automated alerts, and more accurate risk monitoring. For example, smart sensors can detect water leaks or fire hazards early, preventing major damage and simplifying the claims process. By leveraging the Internet of Things and insurance together, insurers can address the inefficiencies of traditional methods, lower operational costs, and boost overall customer satisfaction.

In the following sections, we will explore in greater detail how the Internet of Things and insurance are transforming various aspects of the industry, including its impact on home, auto, health, and life insurance sectors.

The basic idea behind the Internet of Things (IoT) is to link everyday objects to the internet so they can share data and talk to each other. For example, smart thermostats, health trackers, and security cameras collect real-time information, watch over conditions, and send alerts about possible problems. In the insurance industry, this technology, known as IoT in insurance, provides useful insights that help insurers manage policies more effectively.

IoT seamlessly integrates with insurance by embedding smart devices in homes, cars, and health systems. These devices gather data and transmit it to insurers, who use advanced analytics to monitor risks, automate claims, personalize policies, and predict potential issues. This integration of internet of things insurance enhances the efficiency and accuracy of insurance operations. Here’s how it works:

Devices continuously track conditions and report potential risks.

Sensor data verifies incidents, speeding up claims.

Insights from data allow for tailored insurance plans.

Early alerts help prevent damages before they escalate.

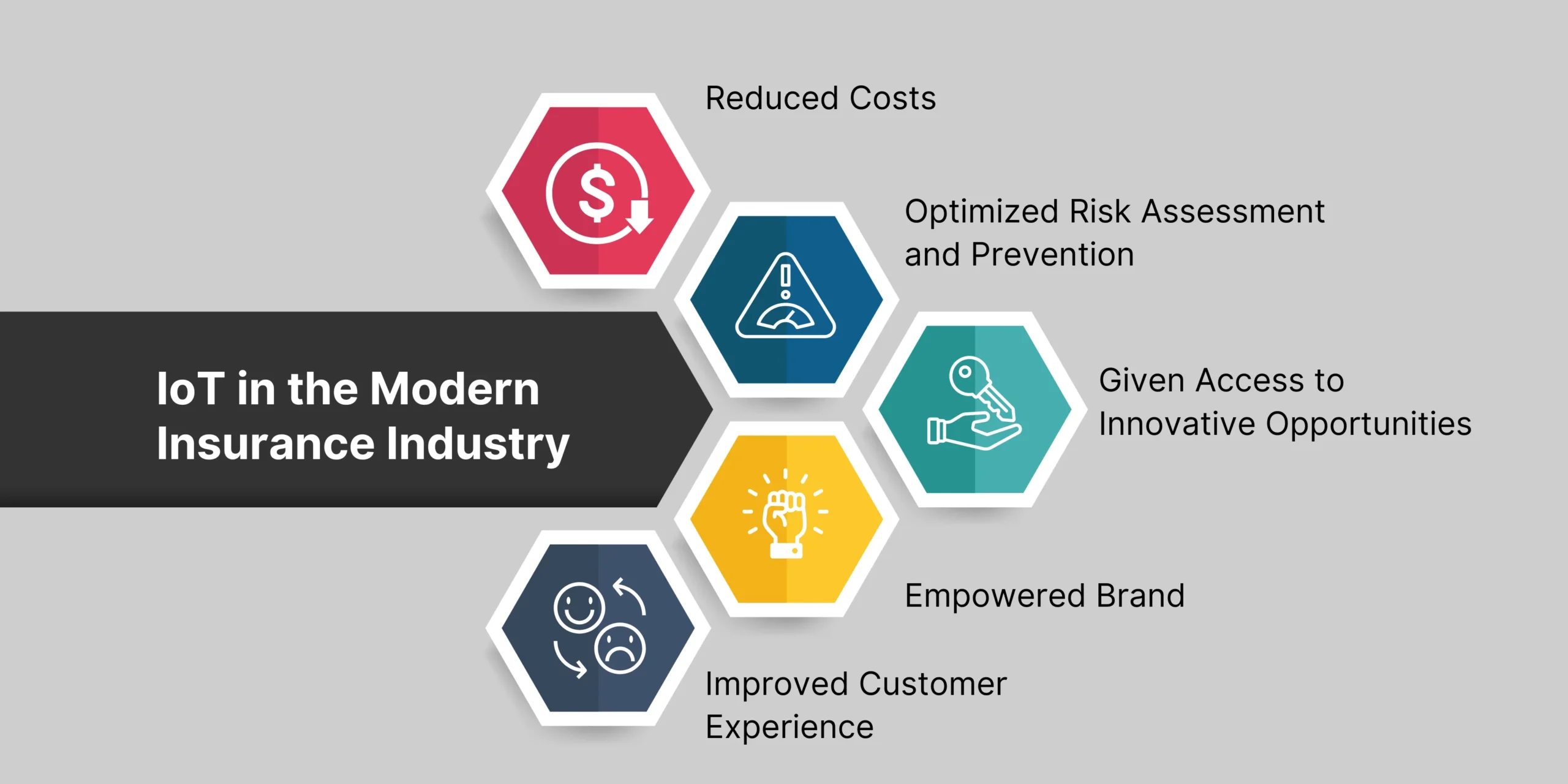

Efficiency: Insurance and IoT are streamlining operations by automating tasks and providing real-time data. For instance, IoT devices like smart home sensors detect leaks or temperature changes and alert homeowners and insurers immediately. This integration of insurance and IoT reduces manual inspections and paperwork, allowing for quicker and more accurate claims processing. Customers benefit from faster service, and insurers save time and resources.

Accuracy : Traditional risk assessments often rely on outdated or incomplete data. IoT devices provide continuous, real-time data, offering an up-to-date view of an asset’s condition. For example, telematics in cars track driving habits, such as speed and braking patterns, providing precise risk assessments. This leads to fairer pricing and better risk management based on actual usage and behavior rather than estimates.

Cost Reduction: IoT technology helps insurers cut costs by enabling proactive measures and reducing fraud. Here’s how:

Automated monitoring reduces the need for human intervention, lowering labor costs

Early detection of issues prevents extensive damage and costly repairs. IoT data can also verify claims, reducing fraud and financial losses.

By integrating IoT technology, insurers enhance operational efficiency, provide more personalized and accurate services, and stay competitive in a rapidly evolving industry.

Use of IoT Devices: IoT devices like leak detectors, security cameras, and smart home systems are transforming home insurance. By integrating IoT and insurance, these devices offer advanced capabilities. Leak detectors can sense water leaks and alert homeowners immediately, preventing extensive water damage. Security cameras provide real-time surveillance, enhancing property security. Smart home systems, which include smoke detectors and thermostats, can monitor various aspects of the home environment and alert users to any anomalies.

1.Early Detection of Issues: With IoT devices, potential problems such as water leaks or fire hazards can be detected early, allowing for quick intervention and minimizing damage.

2. Reduced Damage Costs: By addressing issues promptly, homeowners can avoid extensive repairs, reducing the costs associated with damage claims.

3. Enhanced Security: Continuous monitoring and real-time alerts improve the overall security of the home, deterring burglaries and providing peace of mind.

Implementation of IoT Devices

In auto insurance, IoT devices such as telematics, built-in sensors, and surveillance cameras are making significant impacts. Telematics involves using GPS and onboard diagnostics to monitor driving behaviors like speed, acceleration, and braking. Built-in sensors can track various vehicle parameters and detect issues early. Surveillance cameras can monitor both the driver and the surroundings, providing valuable data in case of accidents.

1.Monitoring Driving Behavior: Insurers can use data from telematics to assess driving habits, rewarding safe drivers with lower premiums and encouraging better driving practices.

2. Reducing Accidents: Real-time monitoring and feedback can help drivers avoid risky behaviors, potentially reducing the number of accidents.

3. Tailored Premiums: By analyzing driving data, insurers can offer personalized insurance plans based on individual driving patterns, making premiums fairer and more accurate.

Role of IoT Devices:

Life and health insurance are being transformed by wearables and remote monitoring devices. Gadgets like smartwatches and fitness trackers track heart rate, physical activity, and other vital signs. Continuous health tracking, enabled by these Internet of Things (IoT) devices, provides insurers and healthcare providers with crucial information. This integration of the internet of things and life insurance helps improve personalized care and risk management.

Real-Time Health Monitoring: Real-time health monitoring is made possible by continuous data gathering, which keeps track of health measurements in real-time and helps with better health management and prompt medical interventions.

Customized Health Plans: Insights from wearables enable insurers to provide health plans that are tailored to a person’s lifestyle and health information.

Early Intervention: Prompt identification of possible health problems guarantees timely medical response, lowering the severity of illnesses and related medical expenses.

Simplifying the Claims Process: Real-time data provided by IoT technology eliminates the need for manual entry, automating the processing of claims. Smart home sensors, for instance, can automatically identify and report water leaks, which expedites the verification of claims and reduces errors.

Enhanced Fraud Detection: By identifying discrepancies, IoT data assists in the identification of fraudulent claims. Telematics data in auto insurance, for example, can identify disparities between reported collisions and real driving behavior, which can drastically lower fraud.

Better Customer Experience: Real-time updates and communication are made possible by IoT devices, which raises customer happiness and transparency. By keeping track of their claims’ progress and getting timely information, policyholders foster loyalty and trust.

The Internet of Things (IoT) is transforming the insurance industry by introducing innovative opportunities and improving risk assessment. Here’s a closer look at how IoT is making a significant impact on the IoT insurance market:

IoT is enabling insurers to adopt usage-based insurance (UBI) models. These models assess risk based on actual behavior rather than relying on general assumptions. This shift results in more accurate risk assessments and fairer premium calculations.

Traditional factors like age and mileage are no longer the sole basis for determining risk. IoT devices collect real-time data on driving speed, route choices, and even mobile phone usage while driving. This detailed insight into customer behavior helps insurers calculate more accurate premiums.

As risk is assessed more accurately, the number of claims decreases, leading to a reduction in overall claim volume. For instance, insurers can offer discounts to drivers who demonstrate safe driving habits through telematics data.

Insurance companies can collaborate with manufacturers of appliances, automobiles, and other products to mitigate actual risks. For example, an insurer might work with a car manufacturer to offer discounts on premiums for vehicles equipped with advanced safety features monitored by IoT devices.

IoT devices provide insurers with real-time data that goes beyond traditional risk factors, offering a deeper understanding of risk.

IoT devices continuously collect data on various factors such as driving behavior, home security, and health metrics. This real-time data provides insurers with a comprehensive view of potential risks, allowing for more precise risk assessment.

With detailed insights into customer behavior, insurers can calculate premiums more accurately. For example, telematics data from a vehicle can reveal safe driving patterns, leading to lower premiums for the driver.

IoT data helps insurers understand customer behavior better. For instance, smart home devices can detect and alert homeowners about potential hazards like water leaks or fire risks, enabling insurers to offer proactive solutions and reduce the likelihood of claims.

IoT is transforming the claims process, leading to enhanced customer satisfaction and increased profitability for insurers.

IoT devices can automatically detect incidents and initiate claims processes. For example, a smart home sensor that detects a water leak can immediately alert the insurer, expediting the claims verification process.

IoT data helps in identifying fraudulent claims by revealing inconsistencies. For instance, telematics data can highlight discrepancies between reported accidents and actual driving behavior.

With real-time data, insurers can respond to claims more swiftly. This not only boosts customer satisfaction but also minimizes the time and resources spent on claims processing.

Insurers must protect customer data from breaches. This involves implementing robust encryption, secure authentication methods, and adhering to privacy regulations to ensure customer information remains safe.

Integrating IoT devices with current systems can be challenging. A solid strategy focusing on cybersecurity, data handling, and legal compliance is essential for a smooth transition.

Setting up IoT infrastructure requires significant initial investment. Insurers should evaluate costs versus benefits to ensure long-term returns.

IoT devices generate vast amounts of data. Effective storage, analysis, and utilization of this data are crucial for improving risk assessments and speeding up claims processes.

IoT can lower insurance premiums by reducing losses. Insurers must adapt their business models, possibly by developing new products or leveraging IoT data innovatively, to stay competitive.

While IoT offers many benefits to the insurance industry, insurers must address challenges related to data security, system integration, costs, data management, and business model adaptation for successful implementation.

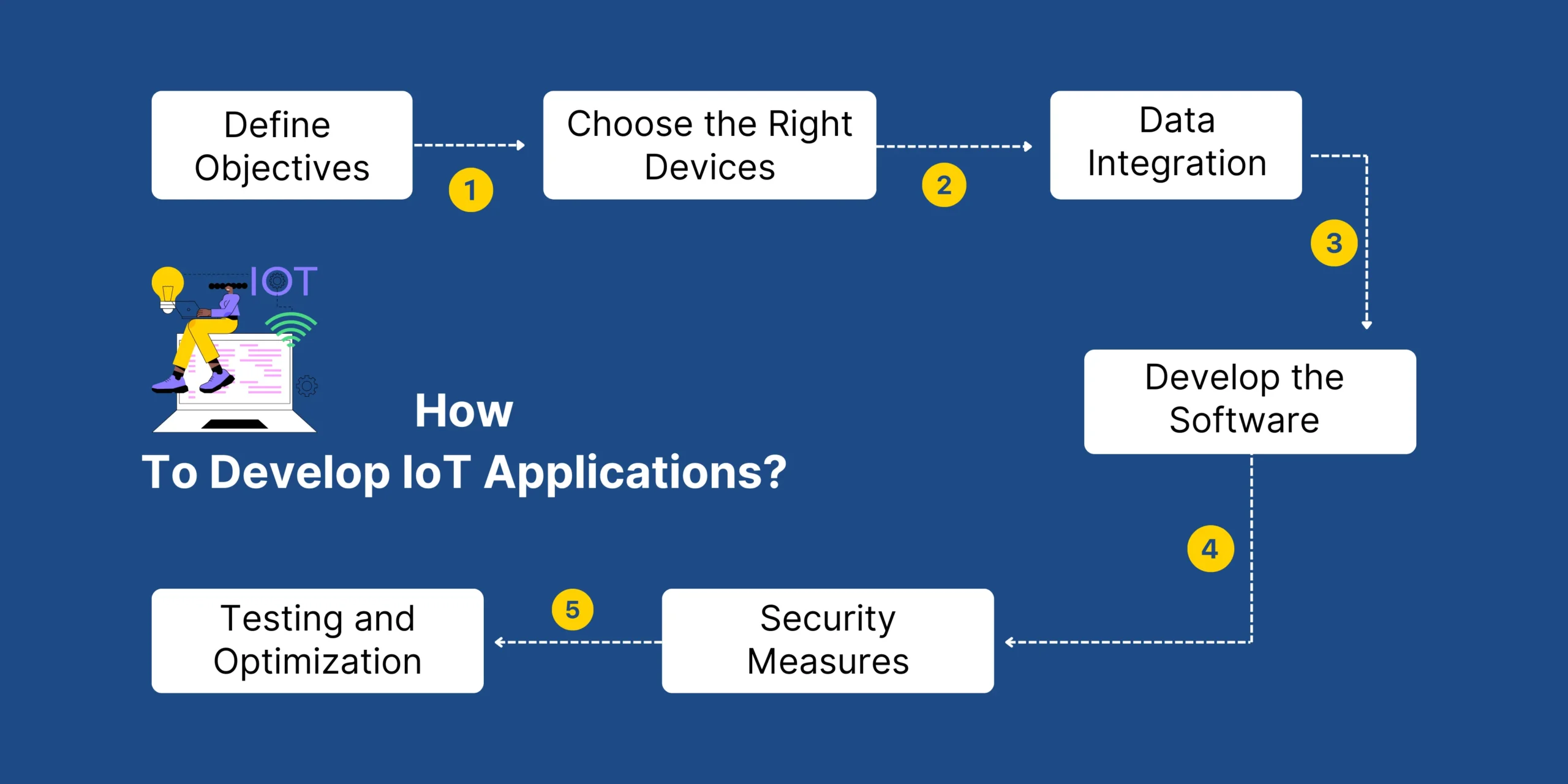

To harness the benefits of IoT in insurance, insurers need to understand how to develop IoT applications that cater to their specific needs. Developing IoT applications involves several key steps:

1.Define Objectives: Identify the specific problems you want to solve with IoT, such as improving risk assessment accuracy or speeding up claims processing.

2. Choose the Right Devices: Select IoT devices that can effectively collect the necessary data, such as sensors, cameras, or wearables.

3. Data Integration: Ensure that the data collected by IoT devices can be seamlessly integrated with your existing systems for real-time monitoring and analysis.

4. Develop the Software: Create software applications that can process and analyze the IoT data, providing actionable insights and automating key processes.

5. Security Measures: Implement robust security protocols to protect the data collected by IoT devices and ensure compliance with regulatory requirements.

6. Testing and Optimization: Test the IoT applications thoroughly to identify and resolve any issues, optimizing performance and reliability.

By following these steps, insurers can develop effective IoT applications that enhance their risk assessment and claims management processes, providing better service to their customers and improving operational efficiency.

For tailored IoT application development solutions, QServices offers expertise in creating advanced IoT applications that meet the specific needs of the insurance industry.

IoT technology is changing the insurance industry by fixing long-standing problems with risk assessment and handling claims. By providing real-time data, IoT devices make the claims process faster and more accurate, reducing costs and improving customer satisfaction. These changes help insurers refine their business models and offer better services.

If you’re curious about how IoT can also boost supply chain visibility and efficiency, check out our previous blog, “Role of IoT in Enhancing Supply Chain Visibility and Efficiency.” It explores how IoT technology can make supply chains work better and improve business performance.

For more information on integrating IoT solutions or if you have any questions, contact QServices. Our team can help you make the most of IoT to transform your business.

Our Articles are a precise collection of research and work done throughout our projects as well as our expert Foresight for the upcoming Changes in the IT Industry. We are a premier software and mobile application development firm, catering specifically to small and medium-sized businesses (SMBs). As a Microsoft Certified company, we offer a suite of services encompassing Software and Mobile Application Development, Microsoft Azure, Dynamics 365 CRM, and Microsoft PowerAutomate. Our team, comprising 90 skilled professionals, is dedicated to driving digital and app innovation, ensuring our clients receive top-tier, tailor-made solutions that align with their unique business needs.

The oil and gas industry works in some of the most challenging and most demanding environments on the planet. From offshore rigs to large refineries, the machinery and infrastructure that powers this sector is extremely important for the global energy supply chain. However, equipment failures can lead to costly downtime, security risks and environmental hazards

Dynamics 365 CRM for Financial Services is a specialized version of Microsoft Dynamics 365 Customer Relationship Management (CRM) tailored specifically for the financial services industry. It is designed to help financial institutions, such as banks, insurance companies, investment firms, and wealth management organizations, manage their customer relationships, streamline operations, and enhance service delivery.

Companies are catching on to the fact that they need cool tech like Dynamics 365 CRM and ReactJS if they want to keep things running smooth and make smarter choices.

Founder and CEO

Chief Sales Officer